Most people approaching retirement have done everything right

individually. The problem is nobody has ever looked at how all of it

works together. One well-meaning decision can quietly cost you thousands

— and nobody sees it until it is too late.

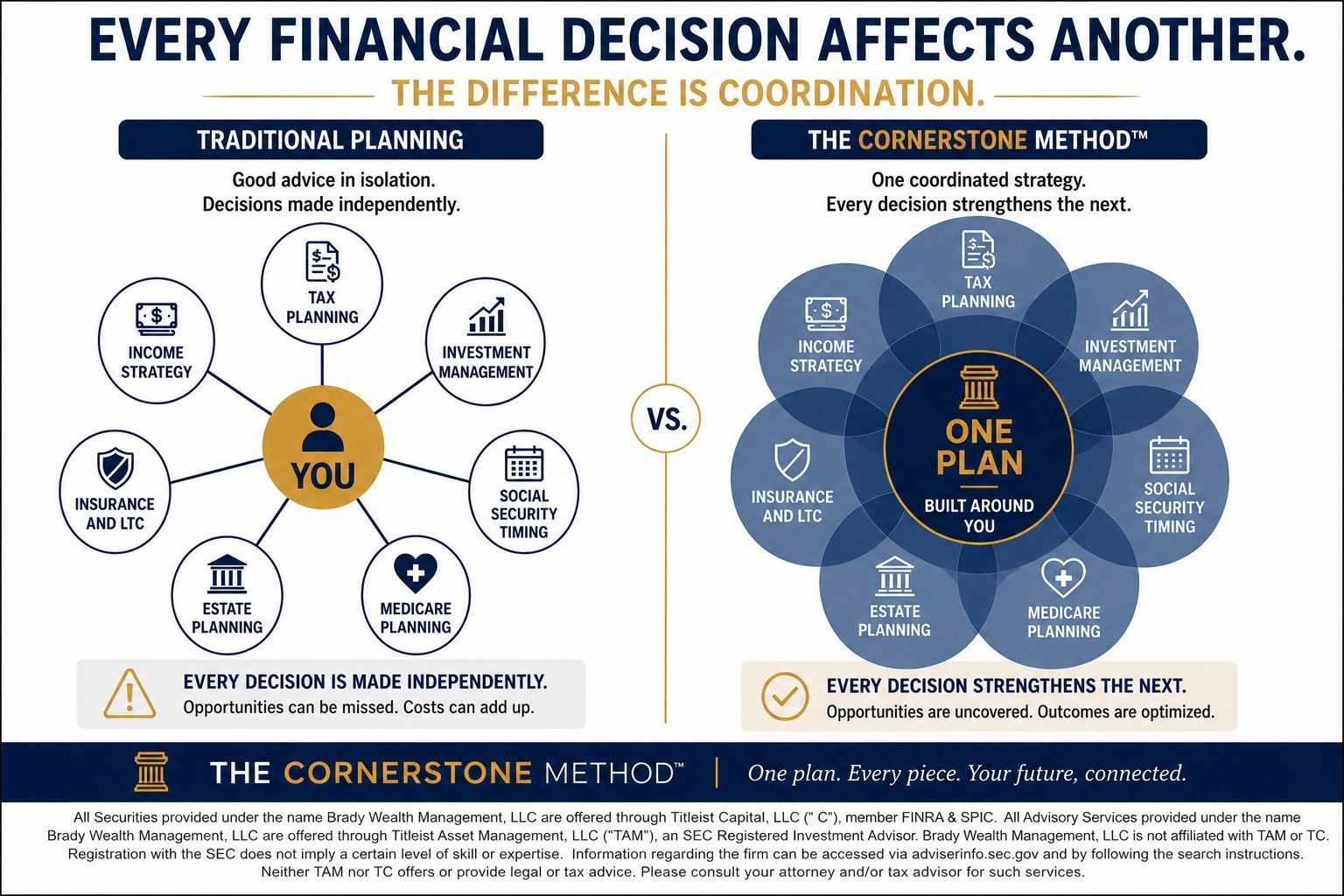

The Cornerstone Plan looks at your complete financial picture — taxes,

investments, Social Security, insurance, estate planning, and income

strategy — all at once. Most people are genuinely surprised by what we

find.

Watch Justin explain exactly what the Cornerstone Plan is, what we typically find, and why it only takes 10 minutes to get started.

Every Cornerstone Plan is built around your specific documents — your actual tax return, your real investment statements, your Social Security record. Nothing generic. Nothing guessed. Everything specific to you. Scroll down to see exactly what we cover and what most people find when they go through this process.

Most people have investment accounts, retirement plans, and tax strategies — but very few have all of those pieces coordinated together. When your advisor, your CPA, and your estate attorney are not talking to each other, gaps appear. The Cornerstone Plan identifies those gaps before they become costly and irreversible — and shows you exactly what it is worth to close them.

Most people tell us the hardest part was deciding to get started. Once they did, it took about 10 minutes.

Here is all we need from you:

Most of these are already sitting in your email inbox or saved on your computer right now. You download them, drag them to our secure upload link, and you are done.

Ten minutes of your time. We do all the analysis. You show up and we show you exactly what we found — including opportunities most people never knew existed.

When was the last time 10 minutes of work could potentially save you thousands of dollars?

Start Your Cornerstone Plan🔒 Your information is kept strictly confidential

Every plan is built around your personal Cornerstone Score — a comprehensive before and after showing exactly where your retirement stands today and where it goes when we implement these recommendations together. The gap between those two scores represents the opportunity we found. Most clients are surprised by how large it is.

How current and future tax law affects your specific retirement accounts — including the exact dollar amount you can convert to a Roth IRA today to lock in lower tax rates before RMDs force larger withdrawals later.

A complete audit of every account — including accounts at other firms — identifying hidden fees, overlapping holdings, and whether your allocation matches where you are in your retirement timeline.

The exact claiming strategy that maximizes your lifetime benefit and your surviving spouse's income — including the specific dollar difference between claiming early versus waiting.

Whether your current income puts you at risk for Medicare premium surcharges — and the specific actions that keep you below the threshold before it is too late to act.

Whether your beneficiary designations match your wishes across every account — because designations override your will and outdated ones can send assets to the wrong person.

Which accounts to draw from first, second, and last in retirement — because the sequence of withdrawals can save tens of thousands in taxes over a lifetime.

A clear before and after showing exactly where your retirement plan stands today and where it goes when we implement these recommendations together. The gap between those two numbers is your opportunity.

Even the most disciplined savers often have gaps they've never seen. Here are the issues we uncover most frequently during a Cornerstone Plan review.

Multiple old accounts sitting at former employers — outdated investments, hidden fees, and beneficiary designations that haven't been reviewed in years.

Large pre-tax balances that will trigger RMDs, push up your tax bracket, increase Medicare premiums, and reduce your retirement income flexibility.

The aggressive strategy that built your wealth may not be right for protecting it. A downturn right before or early in retirement can permanently damage your income plan.

Which account do you pull from first? The wrong sequence can cost tens of thousands in unnecessary taxes over a 30-year retirement.

Claiming at the wrong time can permanently reduce your lifetime benefit — and your spouse's survivor benefit. Most people never see the dollars-and-cents difference.

When RMDs kick in, they can force you to withdraw more than you need — at tax rates you can't control. Proactive planning years in advance can make a dramatic difference.

Healthcare is consistently the most underestimated expense in retirement. We model your exposure to Medicare surcharges, long-term care costs, and out-of-pocket medical spending — so there are no surprises.

When was the last time 10 minutes of work could potentially save you thousands of dollars?

Enter your details below and we'll send you an invitation to schedule your free Cornerstone Plan consultation.